Market analyst outlines trends in embedded OSes, tools

Aug 23, 2005 — by LinuxDevices Staff — from the LinuxDevices Archive — viewsThe embedded OS and tools markets are healthy, driven by robust consumer electronics and telecom sectors, and by innovations such as Linux, Eclipse, and open source, according to Venture Development Corp. (VDC). VDC has published whitepapers on both markets, based on summary findings from its annual study of embedded markets.

The two VDC whitepapers are closely related because, notes VDC, the embedded OS and tools markets converged following their genesis in the early 1990s.

Embedded OSes

Key findings from the VDC report, Embedded and Real-Time Operating Systems include:

- Several factors instrumental in redefining the market and competitive landscape include:

- “Device Software Optimization” (DSO), Wind River's term for off-the-shelf vertical market software/middleware/OS stacks, and related services

- Leveraging open source technology

- Sale campaigns directed at the executive level within “ESMs” (embedded software markets)

- Technology innovation

- VDC estimates that the consumer electronics vertical market continues to be the leading source of revenue for embedded OS vendors, accounting for 41.7 percent of shipments in 2004. Telecom/datacom accounted for 19.7 percent of total market shipments, and ranked as the second largest vertical market in 2004.

- During 2004, the ARM architecture became the leading design supported by embedded operating systems and bundled tools vendors as a percentage of shipments to development teams, increasing to 32.2 percent. Growth continues to be driven by wireless devices across multiple vertical markets and aggressive ARM support for a wide range of embedded and real-time operating systems.

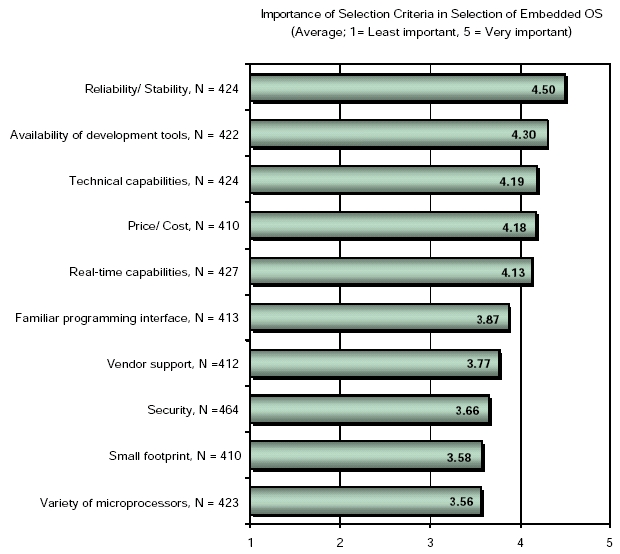

Embedded OS selection criteria

(Click for larger image)

Embedded development tools

Highlights from VDC's report, Embedded Software Development Tools, include:

- Based on recent success, operating system suppliers' strategy to provide their own tools is unlikely to change. The continuously evolving and maturing Eclipse platform has become an effective way for embedded software suppliers to reduce their costs in lieu of developing and maintaining their own proprietary tools or partnering with third-party proprietary tool suppliers.

- Major players in the market have changed their tactical sales focus from project leaders to corporate executives, and are preaching standardization, cost benefits, and device development optimization.

- Availability of free GNU and silicon vendor tools offer a compelling economic proposition, especially to cost-conscious embedded systems manufacturers, presenting a good enough alternative to higher quality tools from standalone tools vendors.

- VDC estimates the Americas region as the largest consuming market for embedded software development tools and related services, with this region accounting for greater than 40 percent of all shipments. However, growth is expected to be faster in the Asia-Pacific region over the forecast period.

- In 2004, VDC estimates the telecom/datacom vertical market as the leading source of revenue for embedded software development tools vendors, accounting for greater than 20 percent of shipments. The military/aerospace market ranked as the second largest vertical market in 2004.

Additional findings from VDC's studies are available in these two downloadable summary findings reports:

This article was originally published on LinuxDevices.com and has been donated to the open source community by QuinStreet Inc. Please visit LinuxToday.com for up-to-date news and articles about Linux and open source.